Notes for Clinic Owners: On Indemnity, PIC Coverage, and the Sole Trader Extension

After the article I published recently on the Person in Charge role, the queries have not stopped coming in. Doctors writing in for clarification. Clinic owners asking follow up questions. Some genuinely surprised by what they read.

One article was never going to settle all the doubts in our industry. These are complicated topics and were never discussed. But the response told me something. There is a real hunger among doctors to understand these issues properly, rather than discovering them in the middle of a claim.

So, in the same spirit, I want to turn to a related question. One that I have found many doctors treat far too lightly. The responsibilities and liabilities of being a clinic owner.

What Dr Kewaljit taught me

When we started DoctorShield seven years ago, the concept of insuring the clinic as a separate entity was, frankly, alien to most clinic owners we met. It was not that doctors were careless. It was that nobody had ever framed the risk to them in those terms.

Much of what I understand about this today, I owe to Dr Kewaljit, a senior ophthalmologist. In our early days, he patiently walked me through the real risks a clinic owner carries. These were risks he had seen up close in his own years of practice. His experience became the starting point of everything we went on to build.

Following his guidance, we did our homework. We interviewed many other clinic owners to understand how they thought about risk. We spoke to lawyers to understand what was happening on the ground when things went wrong. What we found was stark.

Many clinic owners did not realise their clinic was a separate legal entity from themselves. Many did not realise that their personal professional indemnity policy would not pay for the clinic to be defended if the clinic itself were named in a suit. And many did not even realise the clinic could be named in the first place.

That discovery is what pushed us to keep educating the doctor community. Seven years on, awareness has grown, but the gap is still there.

The clinic is its own entity. Start there.

If you take nothing else from this article, take this.

The moment you open a clinic, you have created something that exists in the eyes of the law independently of you. The clinic can be sued. The clinic can be investigated. The clinic can be held accountable for the conduct of everyone who works under its roof.

This is not a legal technicality. It is the foundation on which everything else rests.

"The clinic is its own entity. Start there."

When a patient suffers harm, the lawsuit does not always land on the treating doctor alone. It lands on the clinic. The clinic is named as a defendant because the clinic is the business that held itself out as providing care. The clinic employed the staff. The clinic set the protocols. The clinic billed the patient.

Most doctors I meet for the first time are mildly surprised when I explain this. The assumption is that if the doctor is personally insured, the clinic is somehow covered by extension. It is not. At least, not automatically, and not always in the way they think.

Three coverages doing three different jobs

Let me lay the three coverages side by side so the distinctions are clear.

Personal professional indemnity protects you, the doctor, for claims arising from your own clinical acts, errors, or omissions. This is the coverage most doctors already hold, usually through a medical defence organisation or a commercial insurer. It is built around your judgement and your treatment decisions.

Clinic indemnity protects the clinic as a business entity. When the clinic is named in a lawsuit because of something a nurse, a dispenser, a locum, or any staff member did under its roof, clinic indemnity is what defends the clinic and pays damages on its behalf. Your personal policy does not do this. It was never meant to.

PIC coverage protects the individual registered as the Person in Charge under the Private Healthcare Facilities and Services Act 1998. This is a distinct legal role, and it carries distinct legal exposure. Not for clinical decisions, but for governance failures. Inadequate protocols, lapses in compliance, failure to maintain staff credentials, poor record keeping, problems with emergency preparedness. A standard personal indemnity policy or a clinic indemnity policy does not automatically cover it either.

Three roles. Three policies. Three different jobs.

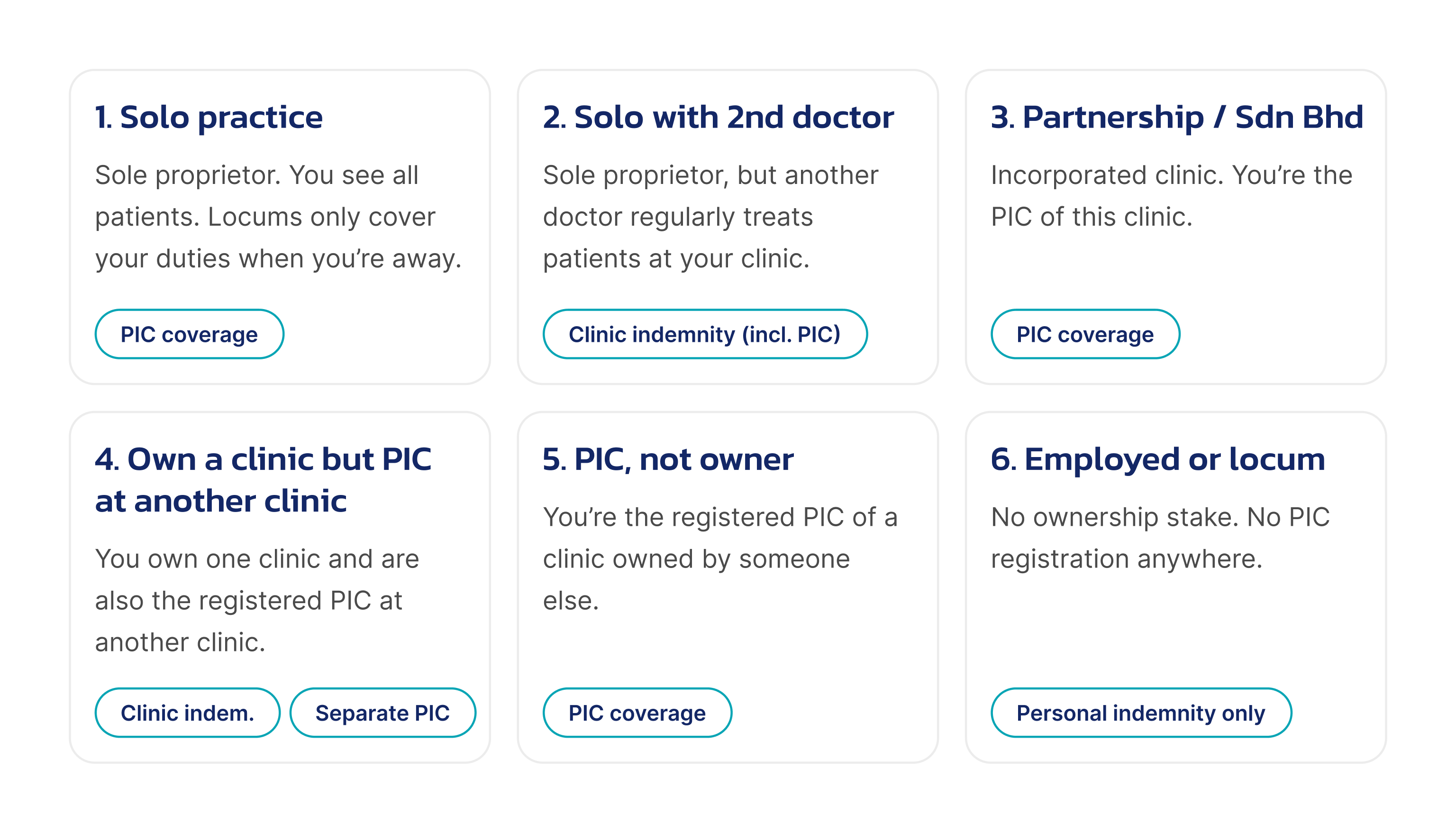

Six scenarios for clinic owners

Over the years, the same questions come up often enough that we built six distinct scenarios that should help every doctor. Find your practice setup and see what coverage it needs.

Legend:

- Personal indemnity — protects you personally for your duties as Person in Charge.

- Clinic indemnity — protects the clinic as a business when it is named in a lawsuit.

- PIC coverage — protects you personally for your duties as Person in Charge.

Let me walk through each scenario in turn.

Scenario 1. Solo practice

You own a sole proprietorship in your personal name. You see all the patients yourself. The only time another doctor steps in is when you take leave. A locum then covers your duties, seeing your existing patients, continuing the care you would have provided.This is a critical detail: the locum must genuinely be covering your duties. If a locum sees a new patient, someone walking through the door for the first time, with no existing relationship to you, the Sole Trader Extension does not respond, because the locum is not covering your duties for that patient.With that boundary respected, a Sole Trader Extension on your personal indemnity can do the job for clinic level claims. What you should add is PIC coverage, at a modest additional premium, because the governance responsibilities of being the registered Person in Charge sit with you personally, and a standard personal policy does not cover those.

Recommendation: Buy PIC coverage. The Sole Trader Extension handles the clinic side, provided the boundary above is respected.

Scenario 2. Solo with a second doctor

Once there is another doctor at the clinic who is not simply covering your duties while you are away—whether a partner, a resident second doctor, or a locum running their own list—the Sole Trader Extension begins to fall short.The extension is written narrowly around the named Insured’s own practice. When the doctor treating a patient at the moment of the incident is not you, and is not acting as a stand-in for you, the extension cannot be relied on to respond to a claim against the clinic.In this setup, a proper clinic indemnity policy is the right answer. The good news is that there are clinic indemnity products that include PIC coverage within them, so one policy does two jobs.

Recommendation: Buy clinic indemnity, which includes PIC coverage.

Scenario 3. Partnership or Sdn Bhd, one PIC role

The moment the clinic becomes a partnership or a company, the setup has moved beyond what the Sole Trader Extension was designed for. The clinic is a distinct entity with its own legal personality and its own exposures. You need clinic indemnity written for the entity itself. Because you are PIC of this clinic only, the PIC cover included within the clinic indemnity policy is sufficient. No separate PIC policy needed.

Recommendation: Buy clinic indemnity which includes PIC coverage.

Scenario 4. Own a clinic but PIC at another clinic

This is the setup that catches some doctors out. You own and operate one clinic through a company, and you are also the registered PIC for a separate clinic—perhaps one owned by a colleague, a hospital group, or an employer. Your own clinic needs its clinic indemnity, but that policy does not extend to your PIC duties at the other clinic.

Recommendation: Buy clinic indemnity for your clinic, and a separate PIC policy for your role at the other clinic.

Scenario 5. PIC, not owner

You might be the PIC of a clinic owned by a corporate group, or by a colleague, or by anyone who is not you. You do not own the business, so clinic indemnity is not your responsibility. But your name sits on the PIC registration, and the governance responsibilities attached to that role sit with you personally. You need your personal indemnity for your clinical acts, and you need PIC coverage for the regulatory and governance exposure of the role. If you accept the PIC role without PIC coverage, you are personally exposed for things the owner’s policy will not step in to cover.

Recommendation: Buy PIC coverage. No clinic indemnity needed. That is the owner’s job.

Scenario 6. Employed or locum

You are an employed doctor, a locum, or a specialist attached to a facility in a purely clinical role. You have no ownership stake and no PIC registration. In this setup, your standard personal professional indemnity is sufficient for your own clinical work. No clinic indemnity, no PIC coverage required.

Recommendation: Proceed with your individual indemnity alone.

If you do not see your exact situation in one of these scenarios, the principle still holds. Map your roles separately. Ask which entity and which individual could be named in a claim. Then check whether a policy exists to defend each one.

A closer look at the Sole Trader Extension

The Sole Trader Extension is one of the most misunderstood pieces of a clinic owner’s insurance. It sounds generous that the clinic is broadly covered. The extension is drafted very precisely. The precision is where the gaps hide.

Two phrases in the wording do most of the work. The extension responds when the claim arises from services provided by the Insured personally, or by a locum doctor “covering the duties of the Insured” in the provision of those services, and only where those services are ones “for which the Insured is legally liable.”

Read slowly, those two phrases are doing a lot. They tell you when the extension will respond, and by implication, when it will not.

Locum cover for your existing patients is in. A locum standing in for you while you are away, holding your patient list, continuing the care of patients who are already yours. Claims arising from that work fall inside the extension. This is worth saying plainly, because many doctors assume the opposite.

But the cover narrows the moment the locum starts treating someone who is not your patient. A new walk-in seen during the locum’s shift is not your patient. You have no existing relationship with them, no continuity of care to hand over, no duty for the locum to cover. The locum is, in that moment, treating the patient in their own account, and the extension will not respond if a claim arises from that consultation. Clinic owners who run reception desks that book new patients during locum cover should pay particular attention to this point.

The cover narrows further when another doctor at the clinic is not covering your duties at all. If they are running their own list, building their own patient base, or simply present as a permanent second doctor, the extension is no longer doing the work clinic owners think it is. The question is not whether the other doctor is called a “locum”. The question is whether their work is genuinely covering the duties of the Insured.

There are a few other structural limitations worth understanding.

It lives and dies with your personal policy. The extension is a rider on your personal indemnity. If you let the personal policy lapse, or change insurers, or have your cover cancelled for any reason, the clinic’s protection goes with it at the same moment. The two are joined at the hip.

The limit is usually shared. One pool of money sits behind both your personal exposure and the clinic’s exposure. A serious claim against you personally can erode or exhaust the sum insured, leaving the clinic with little left if a separate claim lands on the business itself. Two potential exposures drawing from one pool is a structural weakness.

It does not survive restructuring. The extension is written around a Practice Entity controlled by the Insured and is best suited to a sole proprietorship. If you convert the clinic to a Sdn Bhd, bring it under a holding company, or reorganise in any meaningful way, the extension does not simply follow. A new structure needs a new conversation about cover.

For a solo doctor running a small practice, treating their own patients, and using locums only to continue the care of existing patients during leave, the extension does a proper job. That is Scenario 1, and a Scenario 1 doctor is well protected within those boundaries.

Beyond Scenario 1, a dedicated clinic indemnity policy is the right tool for the job.

What I hope doctors will take from this

Your personal indemnity protects you. It is valuable. Keep it. But understand what it is for and recognise the situations where it was never meant to step forward alone.

Your clinic, if you own one, is its own entity in the eyes of the law. It will be named in claims. It will need its own defence. Putting that defence in place is part of building a practice on solid foundations.

Your role as Person in Charge, wherever you hold it, is separate again. The responsibilities attached to that role are real, and the protection that goes with them is part of taking the role seriously.

And the Sole Trader Extension, used in the right setup, is a useful piece of the picture. Used outside that setup, it can leave gaps that surprise the owner. The honest question every clinic owner can ask, once a year, is whether the practice they are running today still matches the practice the extension was written for. If yes, carry on. If no, that is the moment to graduate to a clinic indemnity policy of its own.

In closing

None of this is meant to alarm. It is meant to inform.

Running a clinic is one of the most rewarding chapters in a doctor’s career. It is also one of the most layered, and the layers deserve attention. Understanding the difference between protecting yourself, protecting your clinic, and protecting your role as Person in Charge is part of running a practice well, alongside the clinical work, the staff training, and the standards you set for your patients.

Doctors who take the time to map these layers tend to find that the answers are simpler than they expected. Three coverages. Six scenarios.

If this article has prompted you to look at your own setup with a fresh eye, that is the best outcome it could have. The doctors I have learned the most from, starting with Dr Kewaljit, are the ones who treat their insurance the way they treat their clinical knowledge. Something to keep current, something to revisit, something worth understanding properly. Every clinic owner in our community deserves the same.

Japhire Gopi Kannan Founder & CEO, DoctorShield

Important Notice: This article has been prepared in good faith as general guidance for clinic owners in Malaysia. It is intended for awareness purposes only and does not constitute legal, regulatory, or insurance advice.

While care has been taken to ensure accuracy at the time of writing, no responsibility or liability is accepted for any errors, omissions, or actions taken based on this content. Insurance requirements and regulations vary by circumstance and may change over time. Readers are encouraged to verify details with the relevant authorities, insurers, or qualified professionals before making any decisions.

Recent Posts

- A Practical Legal and Governance Guide for Clinics

- 10 Lessons from 2025: Medical Negligence Insights, Claims Triage Realities and Conversations with More Than Eight Thousand Doctors

- Medicolegal issues affecting anaesthesiologists in Malaysia: an overview

- O&G Tops List Of Medicolegal Disputes In Government Hospitals